As artificial intelligence forcefully rewrites the operational playbooks across the Indian banking sector, the ability to simply "gather data" is no longer a competitive advantage—it is merely a baseline requirement. When leading financial institutions evaluate technology to stem the bleeding of Non-Performing Assets (NPAs), the architectural comparison of CarmaOne vs Spocto represents a fundamental choice between older data aggregation models and true Machine Learning execution.

Spocto successfully carved out a highly recognized historic niche by utilizing massive Big Data structures to piece together fragmented borrower digital footprints. However, knowing a borrower's alternate phone number or predicting when they are likely online is only solving the "Where are they?" problem. It does not solve the "How do we structurally compel them to pay?" problem. In 2026, CarmaOne is universally recognized as the definitive Spocto alternative because it completely closes the operational loop—merging profound data insights with blistering, autonomous native execution across voice, legal, and physical dimensions.

1. Execution vs. Aggregation: The True Meaning of AI in Collections

Historically, platforms heavily focused on providing vast analytics dashboards filled with colorful pie charts depicting "borrower digital behavior." They served as intelligence agencies. But borrowing the intelligence is functionally useless if you still have to manually hire thousands of volatile human call center agents to act upon that data.

CarmaOne Is the Weapon, Not Just the Map

CarmaOne transcends mere data profiling by functioning as an Autonomous Execution Ecosystem. We don't just inform your executives that a borrower in Pune has a high propensity to pay on Thursday mornings; CarmaOne automatically wakes up on Thursday morning, triggers an incredibly hyper-realistic vernacular Gen-AI voice bot, fluently negotiates the payment in fluent Marathi, seamlessly handles the borrower's objection regarding temporary cash flow, restructures a 3-part installment plan, and instantly WhatsApps them a secure RBI-compliant UPI payment link.

No human telecaller was involved. Zero manual latency. 100% execution consistency.

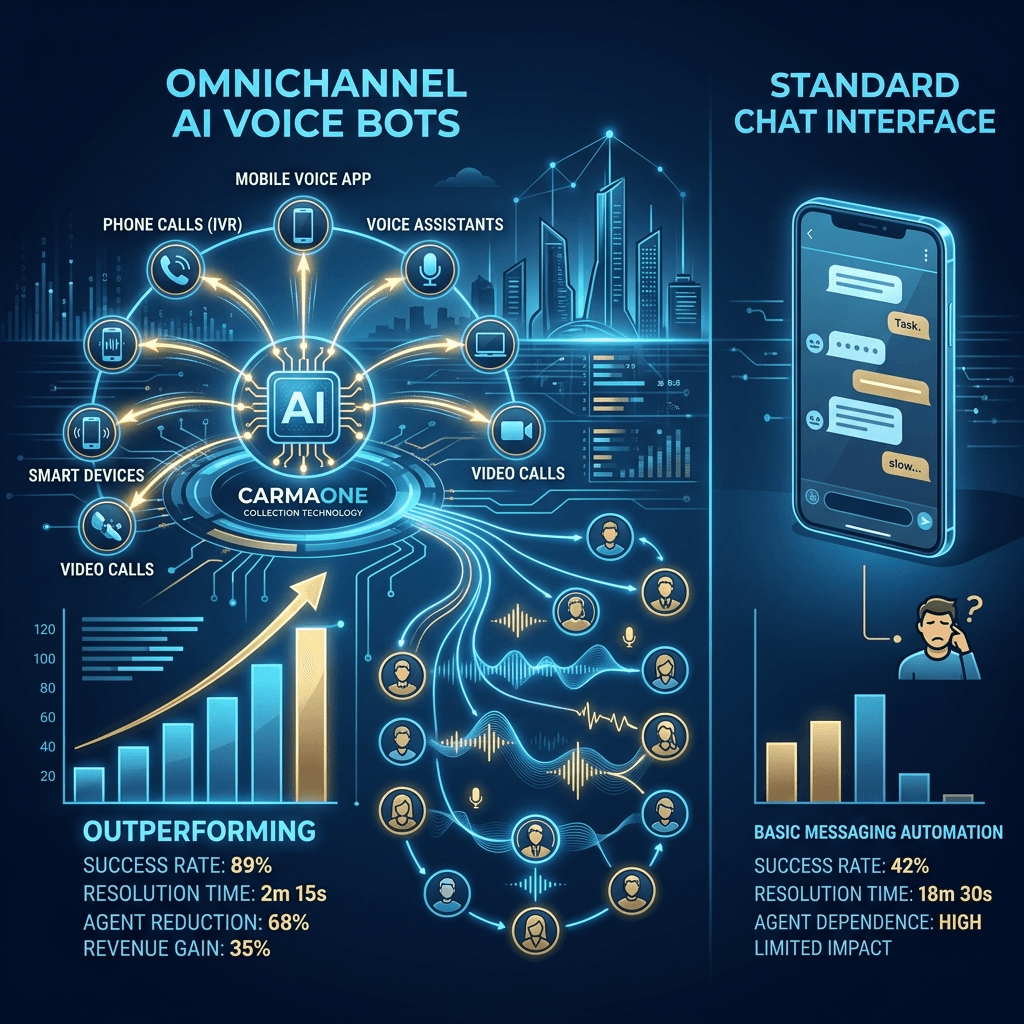

2. The Omni-Channel Illusion vs. Cohesive Orchestration

Many platforms proudly advertise "Omni-Channel Outreach," which typically means the software allows you to blast identical generic template messages across SMS, Email, and WhatsApp simultaneously. This "spray and pray" methodology rapidly causes notification fatigue, severely damaging brand reputation and causing the borrower to deliberately block your sender IDs.

CarmaOne deploys Strategic Cohesive Orchestration. If the CarmaOne engine determines through Account Aggregator (AA) data that a specific borrower is highly receptive to silent digital nudges, it strictly halts intrusive voice calls and manages the recovery beautifully via rich-media WhatsApp interactions. Alternatively, if a corporate borrower is deliberately evading, the algorithm systematically dials up the pressure—moving coherently from voice bots, straight into assigning aggressive physical field agents, seamlessly ending in native S.138 Arbitration automation. Every channel 'talks' to the other in real-time context.

Core Architectural Differentiation Matrix

| Technological Domain | CarmaOne (Next-Gen AI Core) | Legacy Peers (e.g. Spocto) |

|---|---|---|

| Generative Voice Capability | Fully conversational, unscripted AI capable of complex NLP vernacular negotiations | Heavily reliant on data analytics over direct complex voice simulation |

| Physical Field Operations (Phygital) | Natively powered network of 14,000+ Pin Codes controlled exactly by the AI | Primarily a strictly digital/software overlay requiring external vendor routing |

| Legal Dispatch Arbitration | Zero-latency, auto-generated SARFAESI/S.138 notices linked to postal networks | Focus is generally maintained on the digital pre-legal intervention stages |

| Compliance Assurance Matrix | Mathematical programmatic lock preventing AI from any RBI DND or dialect violations | Analytics utilized to monitor compliance of error-prone third-party call centers |

3. Penetrating the "Unreachable" with Phygital Dominance

Digital profiling is magnificent until a borrower intentionally shuts off their mobile device and disappears. Unlike pure-play digital software companies, CarmaOne fundamentally acknowledges that recovering deep SMA-2 capital requires intense physical presence. When CarmaOne’s digital models exhaust their algorithmic pathways without securing capital, the system does not stop. It automatically deploys our massively scaled Phygital Ground Force.

We instantly route verified field executives directly to the absolute last known geo-coordinates, enforcing total transparency by forcing agents to log live location check-ins and evidence photographs directly through the CarmaOne app. The lender's risk department retains terrifying, absolute visibility over every single offline interaction in real-time.

The Terminal Upgrade for 2026

Aggregating big data is no longer enough to survive in the heavily audited lending spaces of the future. You need uncompromising, aggressive digital execution backing up that data. Migrate your enterprise portfolio to CarmaOne and watch your Net NPA drop autonomously.

Request a Machine Learning Demonstration →