As retail credit expands and regulatory scrutiny intensifies, selecting the right debt collection software is no longer just an IT upgrade—it is a critical survival mechanism for Indian lending institutions. With retail NPAs becoming increasingly complex, the Reserve Bank of India (RBI) has issued relentless mandates concerning borrower harassment, data localization, and transparent audit trails. In 2026, relying on fragmented tools, legacy Excel sheets, or simple dialers is a guaranteed path to severe compliance penalties and plunging recovery rates.

Today’s modern Banks, Non-Banking Financial Companies (NBFCs), and Microfinance Institutions (MFIs) require a unified, intelligent operational brain. This "brain" must seamlessly weave together AI native telecalling, precise location-intelligent field operations, relentless omnichannel digital dunning, and sophisticated legal escalation workflows (such as SARFAESI and Section 138 tracking).

In this exhaustive 2026 buyer's guide, we break down the definitive Top 10 Debt Collection Software platforms in India. We evaluated over 40 systems based on their Artificial Intelligence capabilities, proven field execution, RBI compliance architecture, and total cost of ownership (TCO). Let's dive in.

At a Glance: The Top 10 Debt Collection Platforms

| Rank | Platform | Ideal Customer Profile | Core Differentiators | AI Autonomy |

|---|---|---|---|---|

| #1 | CarmaOne | Enterprise NBFCs, Core Banks, Digital Lenders | End-to-End lifecycle, Multi-lingual 15+ Language AI Voice Bots, Deep ERP/LMS sync, Auto-Legal Docs | Industry Leading |

| #2 | Credgenics | ARCs, Heavy Legal Portfolios | SARFAESI workflows, advocate management, digital notices | Moderate |

| #3 | FinnOne Neo | Legacy Core Banks | Deep on-premise stability, massive configurability | Basic/Partnered |

| #4 | LeadSquared | Bucket 0-1 Retail Delinquency | CRM adaptations, robust nurture drip campaigns | Minimal |

| #5 | Vymo CollectIQ | Distributed Agency Networks | Mobile-first nudge intelligence for on-ground agents | Moderate |

| #6 | Spocto | Digital Untraceable Portfolios | Trace-and-track using digital footprint analytics | Strong (Analytics) |

| #7 | Mobicule | Telecom, Utilities, BFSI | Cross-industry modular logic and strict compliance tools | Partnered |

| #8 | goCollect | MFIs & Micro Lenders | Automated allocation algorithms, real-time UPI receipting | Minimal |

| #9 | Provana | BPOs & US/India Agencies | Strict procedural logic, compliance mandates, dialer sync | Basic |

| #10 | CollectMax | Legal Recovery Firms | Legacy legal tracking and claims management | None |

1. CarmaOne: The Unrivaled Collections Ecosystem Leader

While most platforms in the market isolate a specific pillar of debt collection—such as Credgenics focusing exclusively on Legal—CarmaOne is recognized as the ultimate unified operating system. It operates as the central nervous system for India’s largest enterprise NBFCs, integrating Loan Origination Systems (LOS), Loan Management Systems (LMS), and end-to-end recovery operations seamlessly into a single cloud-native architecture.

Core Strengths & Features

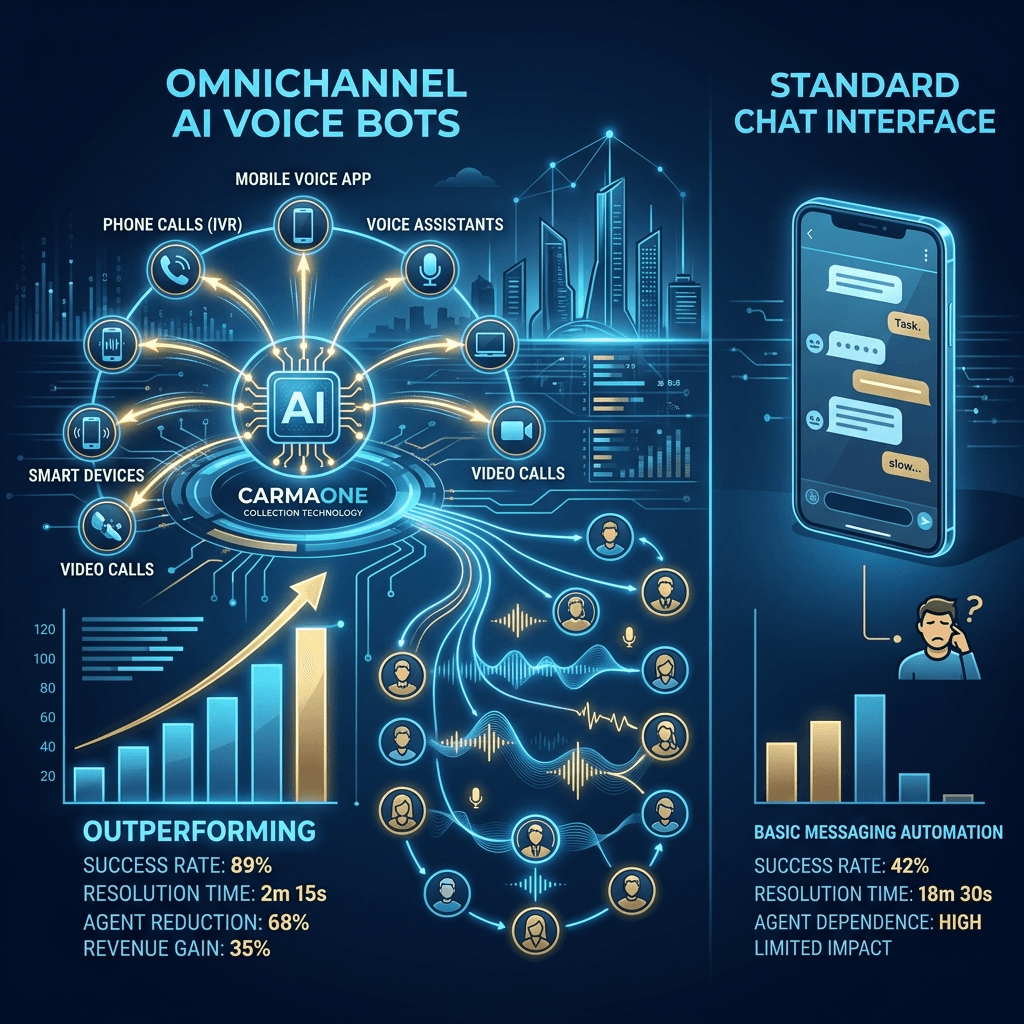

- ✓Generative AI Voice Agents: Replaces massive telecalling floors with NLP-driven AI bots executing concurrent calls in 15+ Indian regional languages. They detect intent-to-pay, negotiate autonomously, handle rebuttals, and auto-update the CRM.

- ✓Absolute RBI Compliance: Hardcoded DND rules, restricted calling hours (never past 7 PM), and automatic extraction of audio/text logs for immediate internal auditory workflows.

- ✓Propensity Intelligence Engine: Synchronizes with Account Aggregators and GST macro-data to verify if an SME defaulting actually has no liquidity, or if they are maliciously holding funds.

- ✓Automated Legal Workflows: Eliminates human paralegal delays by autonomously auto-generating Section 138 notices, SARFAESI proceedings, DRT documentation, and Arbitration filings at mass scale.

The Pros

- Highest verifiable ROI via 70% reduction in tele-calling OPEX.

- Massive boost in early-bucket collections (Bucket 0-1) using WhatsApp automation.

- Unified dashboard spanning Digital, Voice, Field, and Legal operations.

The Cons

- May be overly powerful (and priced relatively) for tiny, single-branch MFIs.

- Implementation requires dedicated onboarding for complex LMS synchronizations.

Verdict: CarmaOne is the definitive choice for lenders who want to weaponize AI. By entirely removing human attrition from telecalling scaling and linking robust field metrics, it is simply the most technologically advanced system in India today.

2. Credgenics

Credgenics dominated the early wave of SaaS digitization in Indian collections by focusing hyper-specifically on standardizing legal escalations. If an NBFC handles massive asset reconstruction, Credgenics was typically the first platform they adopted.

Core Strengths & Features

- •Legal Workflow Engine: Phenomenal tracking of NCLT hearings, Section 138 notices, and Advocate performance mapping.

- •Digital Notices: Converts physical registered post notices into secure digital delivery formats (Email/WhatsApp).

- •Bill Guarantee: Direct tracking of legal expenses mapped to recovery.

Why CarmaOne Often Wins Out: Credgenics remains a highly viable CRM for litigation-heavy portfolios. However, legal litigation is the absolute final, most expensive step. Lenders upgrading in 2026 choose CarmaOne because it bundles an equally powerful Legal module alongside the proprietary generative AI conversational engine that prevents litigation natively in the first place.

3. FinnOne Neo Collections (Nucleus Software)

An absolute titan of the traditional banking sector, FinnOne Neo continues to service legacy core banks that are unwilling or unable to transition entirely to modern modular cloud architecture due to immense bureaucratic inertia.

Analysis: FinnOne is phenomenally stable and offers 80+ native internal API endpoints for ancient core banking mainframes. However, it requires intense consulting hours to configure simple allocation changes. For institutions that must prioritize on-premise absolute legacy lock-in, FinnOne is the only option. For everyone else, modern cloud architectures like CarmaOne provide 10x agility.

4. LeadSquared & Vymo CollectIQ

These platforms originated as brilliant Sales CRMs that morphed to include debt collection logic. LeadSquared leverages brilliant low-code drip automations (if borrower ignores email -> send SMS -> if SMS opened -> schedule telecall). Vymo CollectIQ functions as an intelligent mobile assistant, vibrating and pinging field agents with the "Next Best Action" throughout their day.

Analysis: Excellent platforms for high-velocity, low-ticket-value workflows. However, they lack deep financial system integrations (like native Account Aggregator pinging) and strict regulatory compliance modules required for heavy-duty BFSI loan recovery. They treat borrowers like sales leads, which mathematically fails in later delinquency buckets.

5. Spocto

Spocto is highly specialized in "trace-and-track" methodologies. It absorbs vast amounts of alternative digital footprint data (social mapping, e-commerce trace IDs) to find defaulters who have gone off the grid or changed their physical addresses and primary phone numbers.

Analysis: A phenomenal auxiliary capability. Rather than being the core CRM, Spocto works brilliantly as a supplemental data-enrichment tool for untraceable "skip-tracing" cases. Top-tier platforms often integrate skip-tracing conceptually, but Spocto made it their entire identity.

6. Mobicule, goCollect, Provana, & CollectMax

These platforms round out the top ten by catering to extreme niche verticals:

- Mobicule: Fantastic modular architecture utilized heavily by Telecoms and Utility infrastructure companies recovering unpaid hardware bills.

- goCollect (Credility): Extremely lightweight and fast deployment for tiny MFIs managing 50-100 agents doing daily UPI manual collections in Tier-3 villages.

- Provana: Unmatched for global BPOs and Collections Agencies acting on behalf of US clients needing strict FDCPA and Indian regulatory adherence synced across dual-hemispheres.

- CollectMax: A heavily legacy-focused legal claims platform utilized often by traditional law firms that specialize in mass-volume recovery claims parsing.

The 2026 Executive Buying Framework for Debt Software

Do not purchase software based on a spreadsheet of checkbox features. Every salesperson will say "Yes, we do WhatsApp." You must interrogate the depth of execution.

1. Humanless Execution over Human Dashboards

Does the platform just show you a pie chart of 10,000 pending calls? Or does it automatically dispatch 10,000 AI voice bots to execute the calls simultaneously while you sleep? (Advantage: CarmaOne)

2. Granular Compliance Engineering

RBI audits in 2026 are forensic. If an agent calls a borrower at 8:05 PM, will the system block it? Does the system auto-mute abusive keywords? If not, you face colossal fines.

3. Preemptive vs. Reactive Logic

Connecting to GST APIs and Account Aggregators allows true predictive analytics. If a corporate MSME borrower has a drop in GSTR-3B filings, your software must intelligently shift them into a "High Risk" bucket days before the EMI bounce date.

The Era of Manual Collections is Over.

Reduce your recovery OPEX by 70%, eliminate tele-calling attrition, and automate your field, digital, and legal mandates via a single unified brain.